Caroline Bedale

Using private companies to deliver NHS services means taxpayers’ money is being used to pay for profits to directors and shareholders. Since 2013 decisions on commissioning have been in the hands of Clinical Commissioning Groups (CCGs) which have been required by the 2012 Health and Social Care Act to put an increasing range of services out to tender, but which have also in many cases been keen to privatise services.

A report by the NHS Support Federation in December 2017 found CCG spending an average of 15% of their commissioning budgets on ‘non-NHS providers’ – private companies and charities.

Nor is the problem resolved by use of “non-profit” providers. Large voluntary sector and charity organisations provide a lot of NHS services – and while they don’t make profits or pay dividends to shareholders, their involvement in providing services means that that funding is taken away from the NHS itself and services are fragmented between many providers.

The voluntary/charitable sector should have an important role to play in making sure disadvantaged groups have a big say in their healthcare and in lobbying for better services: but that they should not be providing mainstream NHS healthcare services.

There is also a significant difference between the relatively small amounts paid to local voluntary/charitable sector organisations and much larger amounts to regional/national ones.

Despite devolution in Greater Manchester, where all the councils, which supposedly have a say over the decisions on NHS plans are now run by Labour, the private sector and large voluntary/charitable sector still hold contracts for many healthcare services.

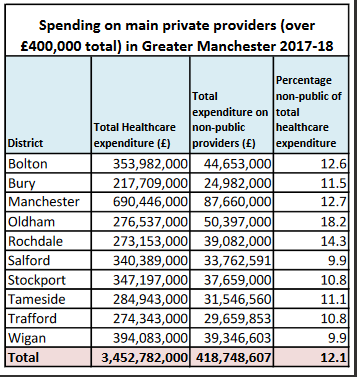

Local campaigners wanting to get a full picture of where public money was being spent made Freedom of Information requests to all the 10 Clinical Commissioning Groups in Greater Manchester (CCGs control the funding for most NHS services), asking for expenditure on services from non-NHS / non-public sector organisations in 2017/18.

This revealed a near 100% variation in the percentage of CCG spending flowing to non-NHS providers, with a lowest figure of 9.9% (Wigan and Salford) and a highest of 18.2% in Oldham. Overall the average was 12.1%, equivalent to almost one pound in every eight going outside the NHS.

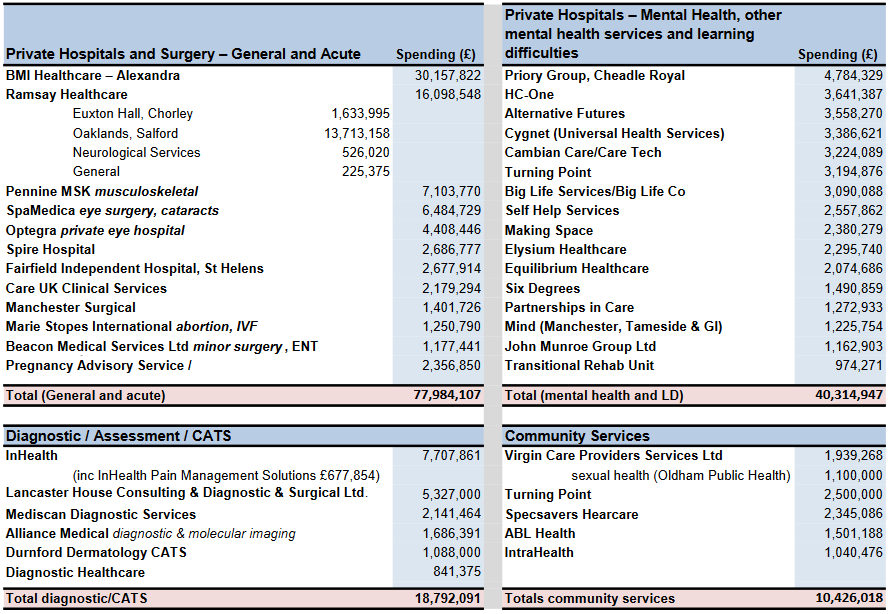

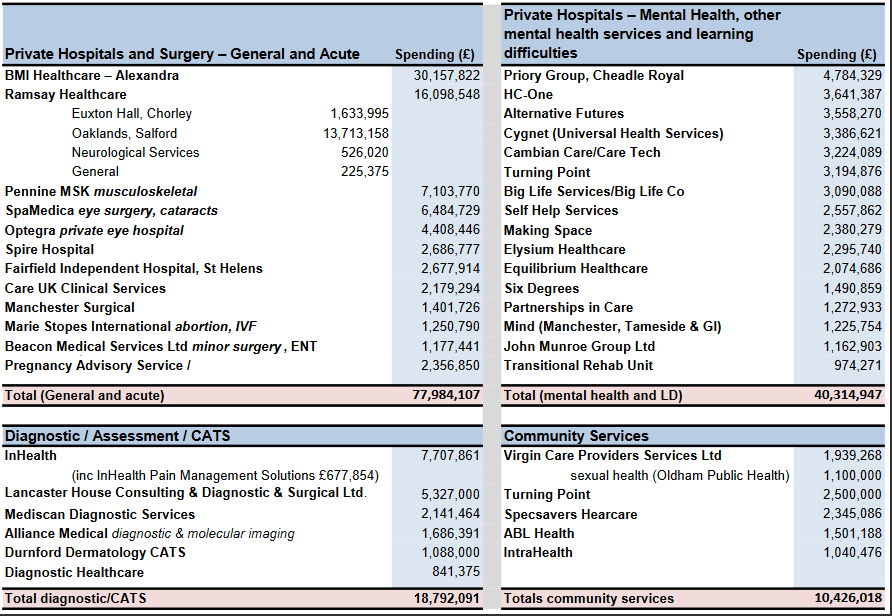

The collated data also reveals the major players among the private providers, with the private acute hospital chain BMI Healthcare the biggest winner, with contracts totalling over £30m, followed by Ramsay Healthcare which picked up over £16m of contracts, the largest share of which went to its Salford hospital, Oaklands.

Two other private general and acute providers, Pennine MSK and Spa Medica (eye surgery and cataracts) were also well ahead of a list of 12 companies or charities gaining more than £1m contract income from Greater Manchester CCGs.

Among the mental health providers, Priory Group (owners of Ticehurst House in East Sussex, where severe failures of care were recently exposed) topped the list with almost £4.8m, followed by the less well-known HC-One (which was formed out of the collapse of Southern Cross, and put up for sale last summer, and has just been fined for a failure of care in a Scottish care home) with £3.6m.

However both would have been eclipsed if the subsequent merger of US-owned Cygnet (owners of the Durham hospital Whorlton Hall, recently exposed by BBC’s Panorama) with Cambian Care/Care Tech had taken place earlier: each company picked up contracts in excess of £3m, and their combined total would have been £6.6m.

Spending on diagnostic services was heavily dominated by InHealth (a company currently in the news for its involvement in a highly controversial PET-CT scanning contract in Oxfordshire) which picked up a total of £7.7m, ahead of Lancaster House with £5.3m.

By contrast with the other services, the scale of contracts awarded for community and public health services are much smaller.

But with a total of £418m flowing out of the CCGs to private providers in Greater Manchester alone in 2017/18, the obvious question is how much better could NHS services be if they were given this extra revenue, and the capital they require to deliver services: and how long can this scale of private spending continue alongside NHS England claims that they want to “integrate” services?

Note on the data

Three of the CCGs, Bury, Manchester, and Stockport would only give the names of private providers but no financial details – saying that ‘commercial sensitivity’ prevents them from giving out this information.

Previously, at the start of the financial year, Stockport had supplied a table listing providers, service type, service description and contract values for 2017/18 – but in many cases actual financial amounts were not given on the basis that they were activity based contracts or AQP contracts, or that it was a framework agreement, or cost per case, so there was no specific contract value. In some cases specific figures were given. Figures in in the section on Stockport are those given in that table of contract values for 2017/18.

However, all CCGs have to comply with a government requirement to publish any payments they make over £25,000 each month, so this data has been used to provide some additional information about the private / voluntary sector expenditure in those 3 districts.

There were sometimes discrepancies between the financial information supplied by some CCGs and the figures in their Annual Reports, but these were not major and do not distort the overall picture.

This analysis focuses on expenditure on healthcare services which are not provided by the NHS or other public sector bodies (mainly local authorities). In the CCG information there are substantial amounts being paid to care homes and home care providers for ‘continuing health care’ (CHC) and ‘funded nursing care’ (FNC). These figures are included in the calculations for total healthcare expenditure.

Dear Reader,

If you like our content please support our campaigning journalism to protect health care for all.

Our goal is to inform people, hold our politicians to account and help to build change through evidence based ideas.

Everyone should have access to comprehensive healthcare, but our NHS needs support. You can help us to continue to counter bad policy, battle neglect of the NHS and correct dangerous mis-infomation.

Supporters of the NHS are crucial in sustaining our health service and with your help we will be able to engage more people in securing its future.

Please donate to help support our campaigning NHS research and journalism.